KYC onboarding software is usually evaluated as an identity verification purchase.

That is only part of the system.

Banks, fintechs, lenders, and other financial-services teams still have to collect customer data, route exceptions, connect verification providers, preserve evidence, and keep sensitive workflows under control. The right question is not only which KYC provider to buy. It is what intake infrastructure the provider connects to.

Key Takeaways

- KYC onboarding software includes identity checks, but the surrounding intake layer matters just as much.

- Dedicated KYC vendors are strongest for document verification, sanctions screening, adverse media, KYB data, biometrics, and verification coverage.

- Form.io is a better fit for the application infrastructure around those checks: embedded forms, structured submissions, generated APIs, permissions, workflows, revisions, audit trails, and customer-controlled deployment.

- Financial-services teams should evaluate who owns the schema, submission record, API handoff, audit evidence, and change-control path.

- The strongest architecture often combines a KYC verification vendor with a governed form platform that controls intake inside the customer's own product and environment.

What KYC Onboarding Software Has To Handle

KYC onboarding is not a simple signup form with a document upload bolted on.

In financial services, onboarding can involve customer identity, beneficial ownership, business entity details, risk indicators, attestations, document evidence, sanctions and PEP checks, adverse media review, manual exception handling, approvals, and ongoing updates.

The fraud pressure behind those workflows is real. The Federal Trade Commission reported that consumers lost more than $12.5 billion to fraud in 2024, a 25% increase from the prior year (FTC). That number does not prove any one onboarding product prevents fraud. It does show why financial-services teams treat identity, intake, and evidence workflows as risk infrastructure.

For covered financial institutions, customer due diligence also extends beyond one-time identity capture. FinCEN describes CDD as policies and procedures that identify and verify customers and beneficial owners, understand customer relationships for risk profiling, and support ongoing monitoring and customer-information updates (FinCEN). FinCEN's 2026 exceptive relief narrowed repeat beneficial-owner verification at every new account opening, but preserved initial verification, risk-based updates, and ongoing monitoring obligations (FinCEN). Digital identity guidance makes the same point from another angle: NIST SP 800-63A-4 defines identity proofing and enrollment requirements across three identity assurance levels, with evidence, validation, and verification expectations that affect onboarding design (NIST SP 800-63A-4). FFIEC authentication guidance also emphasizes layered security and stronger controls than single-factor authentication for financial institution services and systems (FFIEC authentication guidance).

That is the operating reality KYC onboarding software has to support.

It has to help the organization answer:

- What information do we need for this customer type?

- Which evidence is required for this product, jurisdiction, or risk profile?

- Which verification provider or internal service should receive the data?

- Who reviews exceptions?

- Which decisions and changes need to be retained?

- Where does the submission record live?

- How do we update customer information later without losing history?

Those are not only compliance questions. They are application architecture questions.

The Three Layers Of KYC Onboarding Software

Most KYC software pages collapse three different layers into one category.

That makes comparison harder than it needs to be.

1. KYC Verification And Data Providers

This is the layer buyers usually think of first.

KYC verification providers handle identity document verification, database checks, liveness or biometric checks, sanctions screening, PEP screening, adverse media, fraud signals, KYB data, business registry checks, and beneficial ownership data.

If your main problem is global identity coverage, document authenticity, fraud detection, sanctions data, or KYB intelligence, this is the category you should evaluate.

Form.io does not replace that layer.

2. Client Lifecycle And Case Workflow Platforms

Some financial institutions need a broader client lifecycle management system.

That can include onboarding cases, risk scoring, relationship-manager queues, remediation workflows, periodic refresh, monitoring, approvals, dashboards, and enterprise reporting.

If the primary buyer need is a complete CLM suite for a large financial institution, a specialized onboarding or CLM platform may be the right center of gravity.

Form.io does not claim to be a full AML case-management system.

3. Form And Application Infrastructure

This is the layer many comparisons understate.

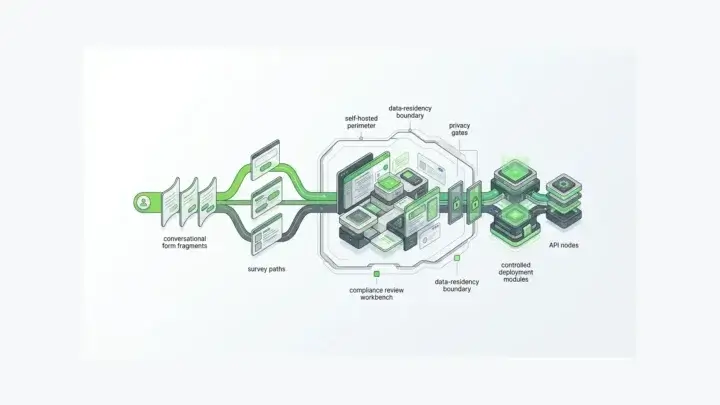

Before a verification service can check anything, the organization has to collect the right data, validate it, structure it, submit it, secure it, route it, and keep the record. That work often happens in forms embedded inside account-opening flows, borrower portals, investor onboarding flows, agent portals, internal review tools, and customer update workflows.

This is where Form.io belongs.

Form.io is not the sanctions database, fraud network, or identity bureau. It is the schema-driven form and API infrastructure that can sit around those systems when the customer needs to own the intake experience and the data path.

Why Static Forms Break KYC Workflows

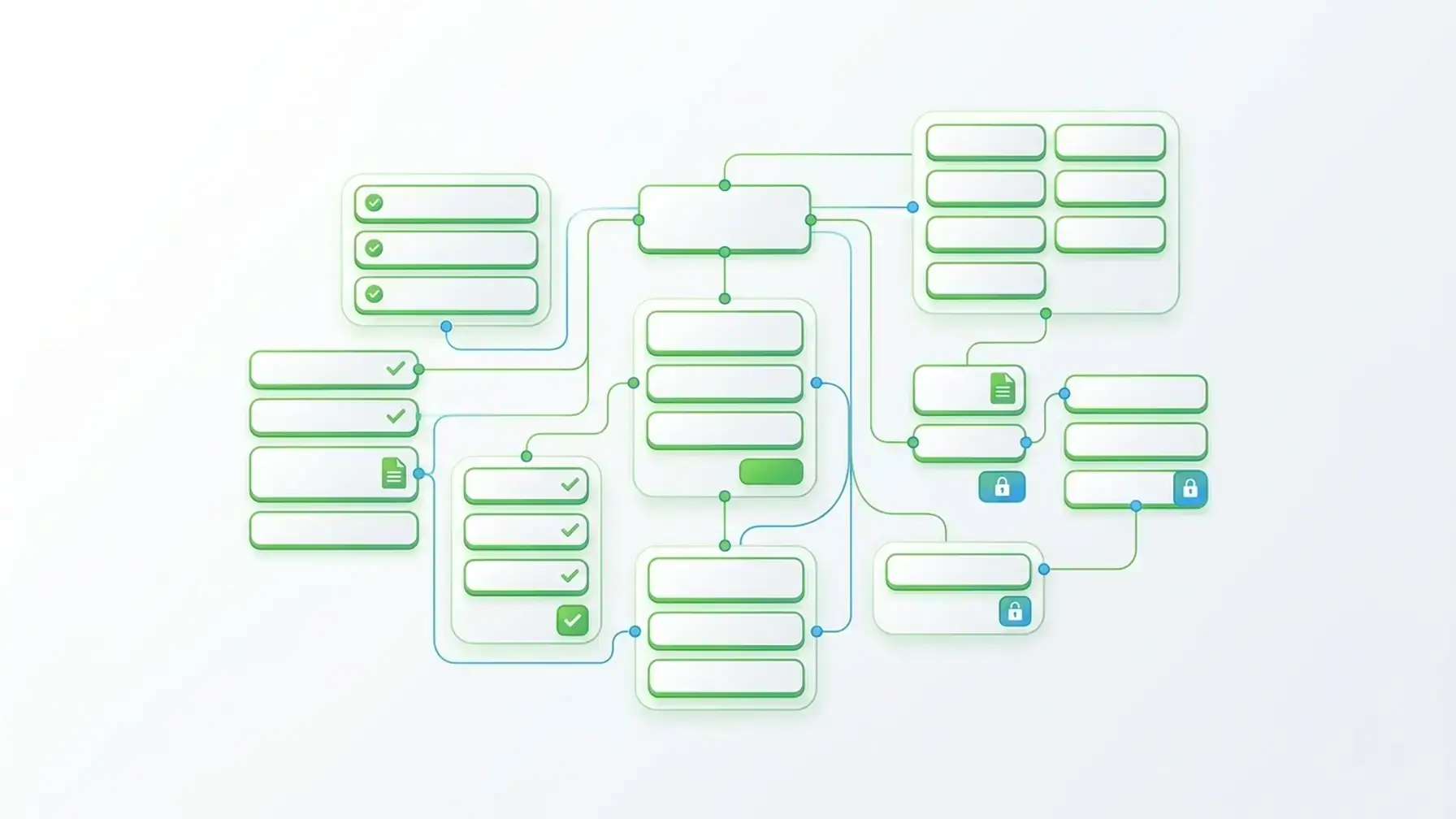

Static forms are comfortable until the onboarding workflow branches.

A retail deposit account does not collect the same evidence as a commercial lending application. A sole proprietor does not require the same entity structure as a multi-owner company. A low-risk domestic customer does not follow the same path as a higher-risk customer, foreign entity, trust, money-services business, or politically exposed person.

KYC onboarding software often has to branch by:

- individual versus business customer

- account or product type

- jurisdiction

- entity structure

- risk level

- ownership profile

- required documents

- missing or inconsistent information

- applicant role

- reviewer role

- periodic refresh or customer update

If those branches live in hard-coded forms, spreadsheets, PDFs, or ad hoc portal logic, the onboarding workflow becomes brittle. Compliance teams cannot change requirements cleanly. Developers cannot route data consistently. Reviewers inherit partial records. Customers get asked for the wrong information.

The stronger model is a governed intake schema: the form defines the data structure, validation, conditional logic, submission record, API handoff, and change path.

That is the Form.io argument.

What A KYC Intake Layer Should Provide

The form layer behind KYC onboarding software should be evaluated as infrastructure, not as a decorative front end.

Dynamic Forms And Validation

KYC intake should adapt to the customer, product, jurisdiction, entity type, and risk profile.

The platform should support conditional logic and validation, reusable components, calculated values, required evidence, document upload fields, consent language, and validation rules. The goal is not to make a long form look nicer. The goal is to collect the right information before the workflow reaches verification, review, or downstream systems.

Structured Submission Records

For KYC, a submitted form is not just a message.

It is a record of what was asked, what was provided, which files were attached, what metadata came with the submission, and what later changed. Submission data needs to remain accessible for internal systems, reviewers, reports, and audit workflows.

Form.io's documentation describes forms as the structure that collects, validates, and stores user data, while the same form structure defines a backend API for managing and accessing submitted data (Form.io docs). That structure matters when KYC data needs to move beyond a form inbox.

API Handoff To Verification And Core Systems

KYC onboarding almost always depends on other systems.

Data may need to move into identity verification providers, sanctions or PEP screening services, CRM, core banking, lending systems, document management, case management, data warehouses, notification tools, and compliance reporting.

For Form.io, the strongest claim is architectural: every form, resource, submission, and project is accessible through a REST API, with predictable endpoints and submission paths that developers can connect to other systems (data integration tools). Webhook actions can also send submission payloads to external endpoints when events occur.

That does not mean Form.io ships every KYC vendor integration out of the box.

It means teams can build the intake and handoff layer around the verification tools they choose.

Role-Based Access

KYC data is role-sensitive.

Applicants, authorized representatives, relationship managers, compliance analysts, operations staff, auditors, developers, and administrators should not all see or edit the same data.

The intake layer should support role and submission permissions around forms, submissions, admin surfaces, and review workflows. This matters because KYC onboarding often blends customer-facing and internal workflows. One weak permission model can turn a controlled process into an overexposed one.

Revisions And Audit Logs

Regulated onboarding workflows need history.

If a customer updates business ownership details, a reviewer changes a risk classification, a required field is added, or an administrator modifies access, the organization needs to know what happened.

Form.io describes two complementary logging systems: Submission Revisions for field-level submission changes and Server Audit Logging for system activity such as form access, authentication, and API-level data modifications (audit trail capabilities). Those capabilities fit KYC intake because the evidence trail is part of the workflow, not an afterthought.

Availability and configuration still matter. Teams should confirm which modules, settings, and license terms apply before making compliance commitments.

Deployment And Data Boundary Control

KYC onboarding touches sensitive personal and business information.

Some financial-services teams can use hosted tools without issue. Others need stricter control over environment, authentication, database, file storage, network access, logging, and vendor exposure.

That is where self-hosted forms or customer-controlled deployment becomes part of the buying decision. Form.io is strongest when the intake layer needs to live inside the customer's architecture rather than as a disconnected third-party form surface.

How Form.io Fits Beside KYC Verification Vendors

The right architecture is often not Form.io instead of a KYC vendor.

It is Form.io around the KYC vendor.

A financial-services team might use Form.io to build an embedded onboarding flow that collects customer and entity data, validates required fields, captures documents, stores submissions, applies role-based access, and exposes the submission through APIs. The same workflow can then call identity verification, document verification, sanctions screening, fraud, CRM, or core system services.

That division of responsibility is clearer and more credible:

| Layer | What It Does | Typical Fit |

|---|---|---|

| KYC verification provider | Identity proofing, document checks, sanctions or PEP screening, KYB data, fraud signals | Use when verification intelligence and coverage are the core need |

| CLM or onboarding suite | Cases, queues, lifecycle workflows, risk review, remediation, dashboards | Use when the institution needs a broad onboarding operating system |

| Form.io intake infrastructure | Embedded forms, structured submissions, generated APIs, permissions, revisions, audit trails, workflow handoff, self-hosted deployment | Use when the team needs to own the intake layer inside its product and systems |

This distinction also keeps the compliance claim honest.

Form.io can support regulated KYC onboarding controls. It does not make an organization compliant by itself. It does not replace AML policy, compliance staff, model validation, legal review, sanctions data, transaction monitoring, or the specialized identity providers that verify people and businesses.

It gives teams the form/application layer those systems need to receive clean, structured, governed intake data.

KYC Onboarding Software Evaluation Checklist

When evaluating KYC onboarding software, ask who owns each part of the workflow.

| Evaluation question | Why it matters | What to check |

|---|---|---|

| Who owns the intake schema? | KYC requirements change by customer type, product, jurisdiction, and risk profile | Form definitions, reusable components, conditional logic, validation, versioning |

| Can the workflow collect documents and evidence? | Verification and review often depend on file evidence | Secure uploads, metadata, submission association, downstream access |

| Does the submission have an API? | KYC data needs to move into verification, CRM, case, banking, lending, and reporting systems | REST APIs, webhooks, JSON submissions, authentication, retry/error patterns |

| Can permissions be scoped by role? | Applicants, reviewers, admins, and auditors need different access | Form permissions, submission permissions, own/all access, SSO role mapping |

| Is the workflow auditable? | Reviewers need to understand changes and decisions | Submission revisions, form revisions, audit logs, timestamps, user identity, notes |

| Can the system support ongoing updates? | KYC and CDD are not always one-time events | Customer refresh flows, changed-information capture, reviewer routing, historical records |

| Can the intake live inside your product? | Customer onboarding often belongs inside a portal or application | Embedded renderer, white-label controls, developer-owned front end |

| Can the environment be controlled? | Some teams need strict data boundary and infrastructure control | Self-hosted or customer-controlled deployment, database/storage options, logging integration |

| Does the product overclaim compliance? | Software supports controls; it does not replace legal obligations | Clear scope, configuration details, module requirements, evidence of controls |

The checklist helps separate a strong verification tool from a strong intake platform.

Some buyers need both.

When A Dedicated KYC Vendor Is The Better Fit

Use a dedicated KYC vendor when the primary need is verification intelligence.

That includes:

- identity document verification

- biometric or liveness checks

- sanctions, PEP, and adverse media screening

- KYB data and business registry checks

- beneficial ownership data services

- fraud network signals

- country-specific document coverage

- transaction monitoring or AML case management

Those are specialized capabilities. A form platform should not pretend to replace them.

The same is true for a full client lifecycle suite. If the institution needs enterprise case management, risk scoring, remediation workflows, onboarding dashboards, periodic refresh operations, and compliance-team queues in one packaged system, a CLM platform may be the better center of gravity.

Form.io becomes more relevant when the organization already has or plans to choose those systems, but still needs to own the form layer that feeds them.

Where Form.io Is The Better Fit

Form.io is the better fit when the KYC onboarding workflow is also a product, integration, and governance problem.

That usually means:

- onboarding forms need to be embedded inside a customer portal or internal product

- the data model needs to be controlled by the application team

- submissions need to become API-accessible records

- KYC providers need to be called from the workflow rather than own the whole experience

- permissions need to be scoped across applicants, reviewers, admins, and service accounts

- form and submission changes need revision history

- audit logs need to feed operational or compliance tooling

- sensitive intake data needs to remain in customer-controlled infrastructure

- teams need one governed form layer across multiple onboarding use cases

That is the buyer who should evaluate Form.io as part of a KYC onboarding software stack.

A Trustpilot reviewer called Form.io a "powerful embedded form builder" and wrote that it was "seamlessly built into our B2B application" (Trustpilot). That is a small proof point, but it points at the right fit: Form.io is strongest when developers and regulated teams need data management, integration, and control around forms, not just a hosted questionnaire.

Bottom Line

KYC onboarding software is not one product category.

It is a stack.

Verification vendors help confirm identity, screen risk, and supply data. CLM platforms help manage onboarding cases and lifecycle operations. Form infrastructure governs the intake layer: what gets asked, how it is validated, where the submission lives, which systems receive it, who can access it, and what evidence remains when the process changes.

For financial-services teams, that layer deserves its own evaluation.

If the problem is buying verification coverage, choose a KYC provider. If the problem is owning regulated intake across products, portals, APIs, reviewers, audit trails, and customer-controlled infrastructure, evaluate Form.io as the form/application infrastructure around the KYC workflow.

FAQ

What is KYC onboarding software?

KYC onboarding software helps financial-services teams collect customer information, verify identity, assess risk, route exceptions, and preserve records during account opening or customer onboarding. The category can include identity verification tools, KYB providers, CLM platforms, and form/application infrastructure. Buyers should separate those layers before comparing vendors.

Is Form.io a KYC verification provider?

No. Form.io is not an identity verification bureau, sanctions database, biometric provider, AML case-management system, or KYB data provider. It can provide the embedded form, submission, API, permissions, and workflow infrastructure around those services.

Where does Form.io fit in a KYC onboarding stack?

Form.io fits at the intake and application-infrastructure layer. Teams can use it to build embedded onboarding forms, collect structured data, manage submissions, connect APIs and webhooks, scope access, preserve revisions, and deploy in customer-controlled environments. Dedicated verification vendors can still handle identity checks and screening.

Why are forms important in KYC onboarding?

The form layer determines what information is collected, how it is validated, how it is stored, and how it moves into downstream systems. Weak forms create incomplete data, manual rework, inconsistent review paths, and poor audit evidence. In KYC workflows, form design is also data architecture.

What should financial-services teams look for in KYC intake software?

Look for dynamic forms, conditional logic, document upload support, structured submissions, API access, webhooks, role-based permissions, revision history, audit logging, authentication integration, and deployment control. Also confirm what the product does not do, especially around legal compliance, AML policy, sanctions data, and identity verification.

Can Form.io help with beneficial ownership collection?

Form.io can help teams build intake workflows that collect business entity and beneficial ownership information, validate required fields, store submissions, and route data to review or verification systems. It does not determine the legal obligation by itself. Teams should map fields and processes to current regulatory counsel and compliance requirements.

Can Form.io connect to KYC or AML vendors?

Yes, Form.io is built for API-connected form workflows. Forms and submissions can be exposed through REST APIs, and webhook actions can send submission data to external systems. Teams still need to implement and govern the specific integration with their chosen KYC, AML, CRM, banking, or case-management systems.

Does Form.io make a financial institution compliant?

No software makes a financial institution compliant on its own. Form.io can support regulated onboarding controls through structured intake, permissions, APIs, revisions, audit logging, and customer-controlled deployment. Compliance still depends on policy, configuration, monitoring, staff judgment, legal review, and the broader control environment.

When should a team choose a full KYC platform instead of Form.io?

Choose a full KYC platform when the main need is identity verification coverage, fraud signals, sanctions screening, KYB datasets, adverse media, transaction monitoring, or packaged case workflows. Choose Form.io when the main need is to own the embedded intake layer and connect it to those specialized services.

Is self-hosting important for KYC onboarding software?

It depends on the organization's risk posture, architecture, and regulatory environment. Some teams can use hosted KYC products. Others need more control over data, authentication, file storage, logging, network boundaries, and deployment. Form.io is relevant when customer-controlled infrastructure is part of the requirement.

How should teams start evaluating Form.io for KYC onboarding?

Start by mapping the intake workflow: customer types, fields, documents, verification calls, exception paths, reviewer roles, submission records, audit needs, and downstream systems. Then evaluate whether Form.io can provide the governed form and API layer around the verification tools the organization already uses or plans to adopt.

Build controlled onboarding workflows with Form.io.

Try Form.io for free